Capital Bikeshare is operated by LYFT, a popular ridesharing company. While their main business is ridesharing and not bikesharing they do provide bikesharing services for many large cities in the US in addition to electric scooters. Without their investment into bikesharing it would be difficult for these cities to provide this service to its residents. Therefore, I found it of interest to attempt to model the volatility clustering of their stock returns to get a better understanding of their financials.

Code

# Set the start and end dates for the time period you want to analyzestart_date <-"2018-01-01"end_date <-"2023-04-04"# Download the Lyft stock datagetSymbols("LYFT", src ="yahoo", from = start_date, to = end_date)

[1] "LYFT"

Code

# Calculate the daily returnslyft_returns <-dailyReturn(LYFT)# Print the first few rows of the daily returns datahead(lyft_returns)

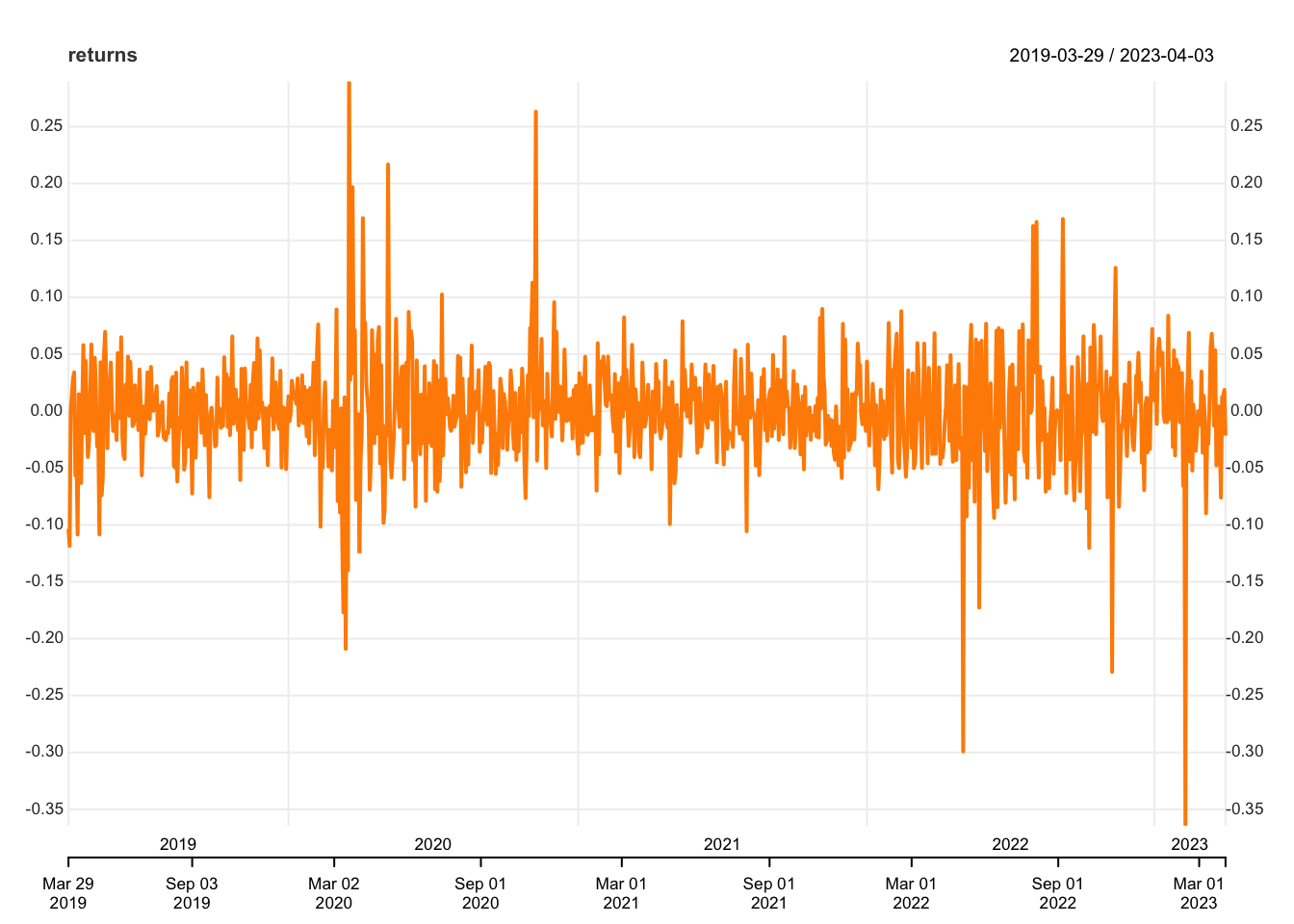

The Daily Returns plots shows clear volatility clustering. There are multiple periods in the time frame where there is a high volalitly period followed by lower volatility. This makes this series a good candidate for arch/garch modelling.

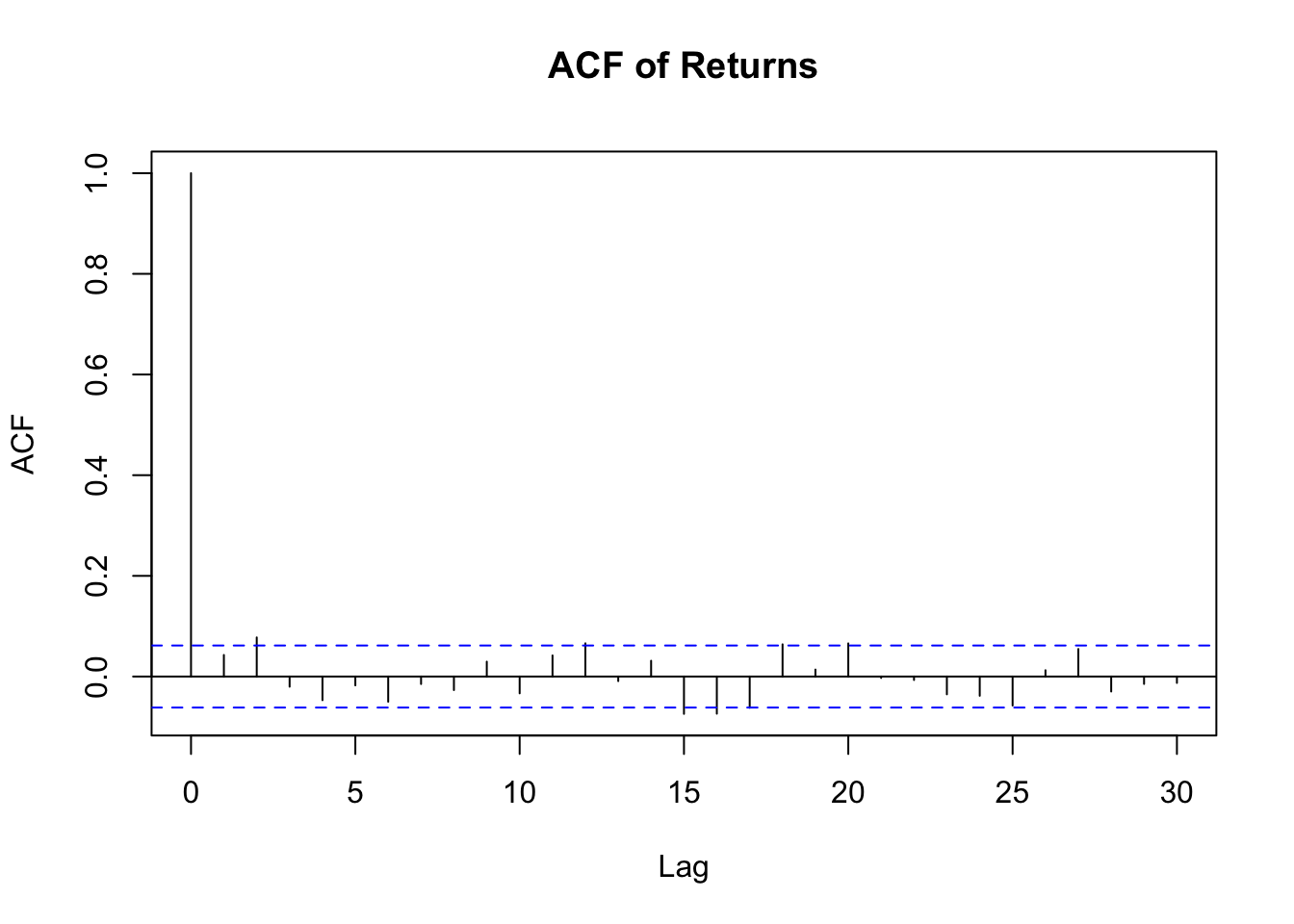

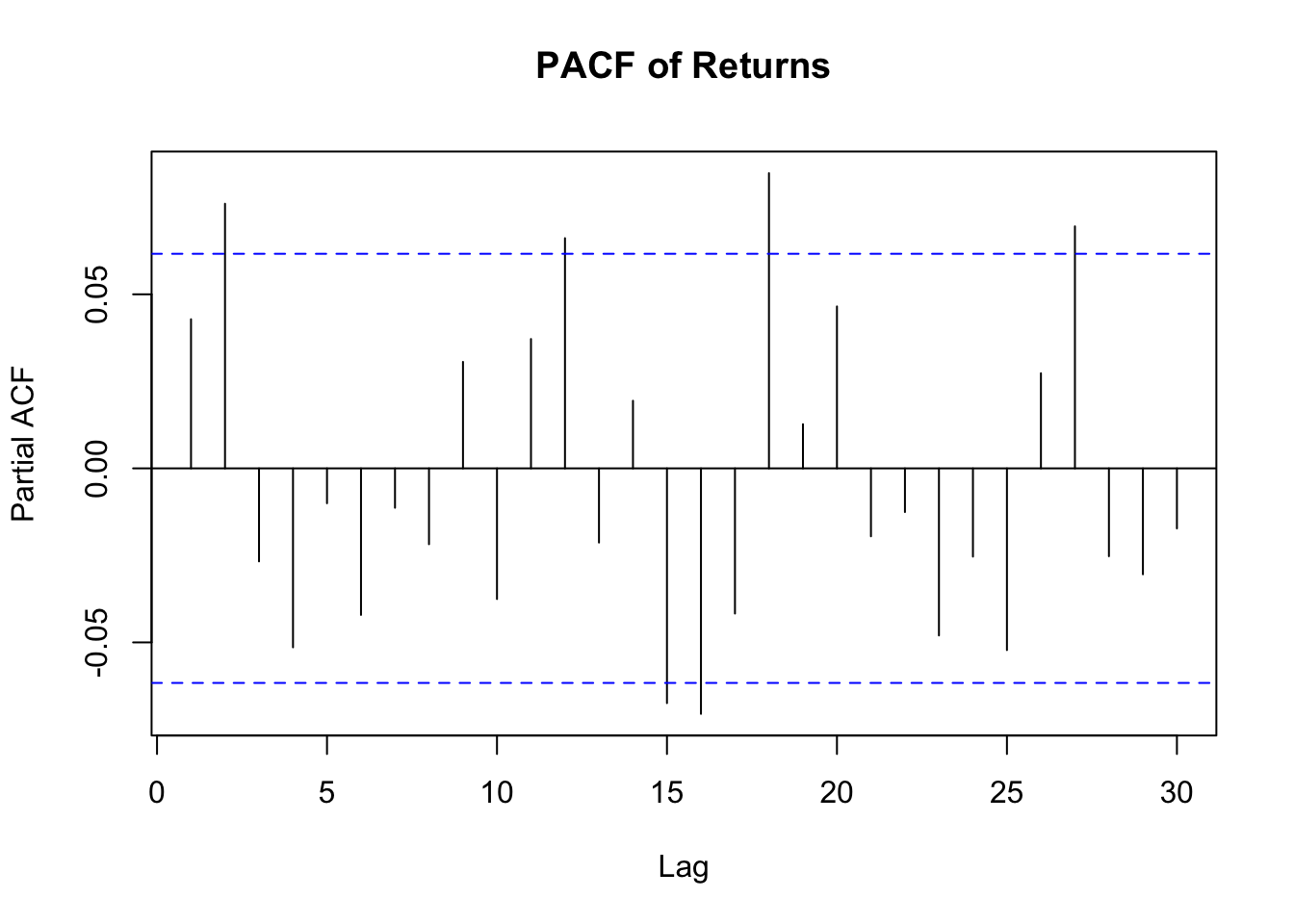

The acf and pacf of the reutrns data both show significant correlation at the first few lags indicating that an arma model is likely suitable for this data. The series doesn’t appear to need differencing but we will check if ARIMA models perform better as well.

Code

acf(returns, main ="ACF of Returns")

Code

pacf(returns, main ="PACF of Returns")

Optimal ARIMA Model

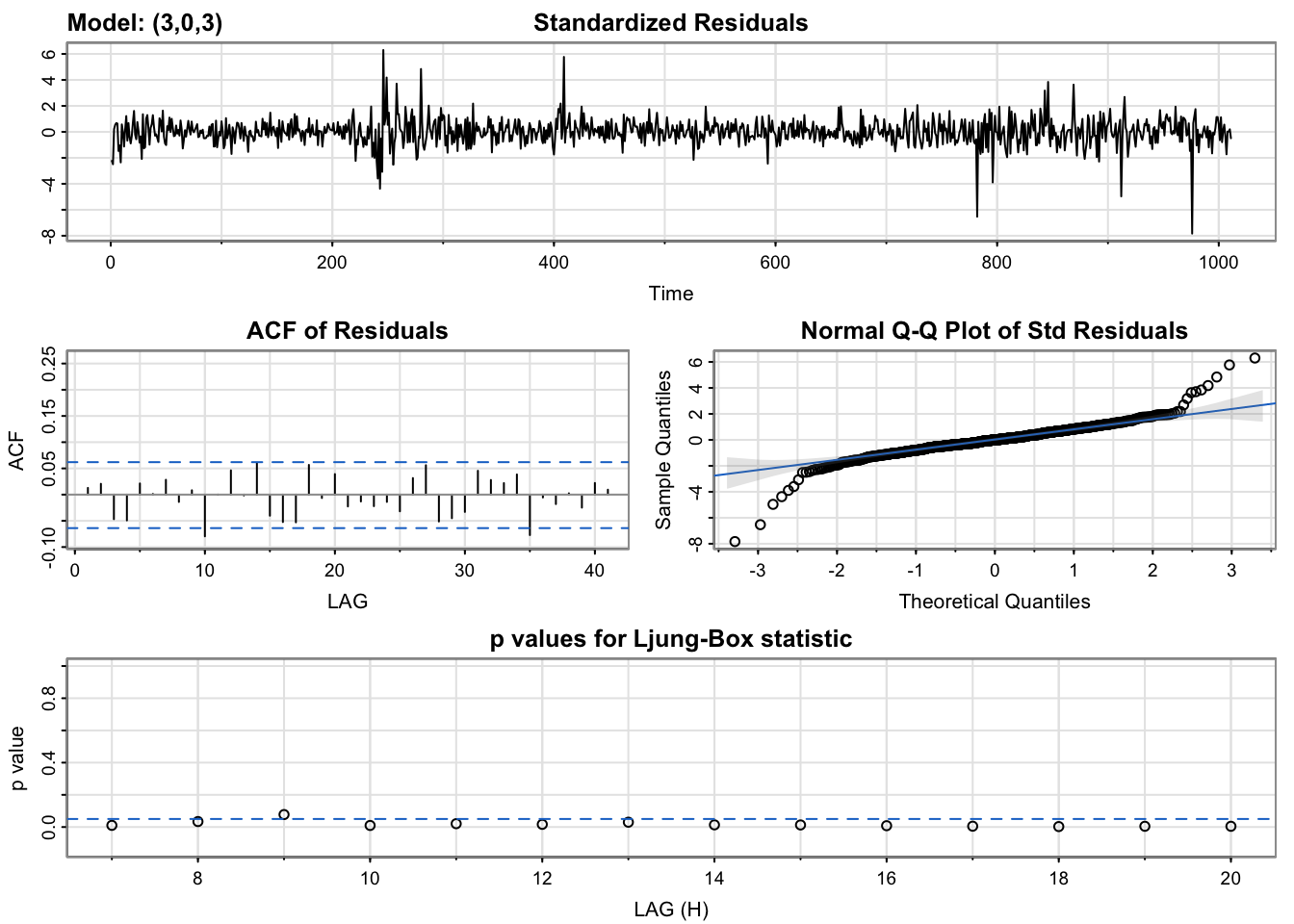

By comparing different values of p,d,q the optimal model based on AIC was found to be an arma(3,3).

Code

optimal_arima <-function(data, max.p, max.d, max.q) {# data: a vector or time series object of your data# max.p: the maximum order of the autoregressive (AR) term# max.d: the maximum order of differencing# max.q: the maximum order of the moving average (MA) term# Create a dataframe to store the results results <-data.frame(p =integer(), d =integer(), q =integer(), AIC =double(), BIC =double())# Calculate the AIC and BIC for each ARIMA(p,d,q) model with p <= max.p, d <= max.d, and q <= max.qfor (i in0:max.p) {for (j in0:max.d) {for (k in0:max.q) {if (i ==0&& j ==0&& k ==0) {next }if (i + j + k >8) {next } model <-Arima(data, order =c(i, j, k)) aic <-AIC(model) bic <-BIC(model) results <-rbind(results, data.frame(p = i, d = j, q = k, AIC = aic, BIC = bic)) } } }# Return the results dataframereturn(results)}results =optimal_arima(returns, 5,3,5)results[which.min(results$AIC),]

p d q AIC BIC

71 3 0 3 -3375.366 -3336.016

Optimal Model Diagnostics

The diagnostics for this model are not great, still showing significant autocorrelation.

Code

fit =Arima(returns, order =c(3,0,3))summary(fit)

Series: returns

ARIMA(3,0,3) with non-zero mean

Coefficients:

ar1 ar2 ar3 ma1 ma2 ma3 mean

0.8664 -0.0034 -0.6061 -0.8523 0.0454 0.5924 -0.0012

s.e. 0.4229 0.6271 0.3986 0.4353 0.6351 0.4148 0.0015

sigma^2 = 0.002058: log likelihood = 1695.68

AIC=-3375.37 AICc=-3375.22 BIC=-3336.02

Training set error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 2.197294e-05 0.04521095 0.03146807 Inf Inf 0.6945023 0.01280739

Code

sarima(returns, 3,0,3)

initial value -3.089163

iter 2 value -3.089626

iter 3 value -3.093328

iter 4 value -3.093348

iter 5 value -3.093377

iter 6 value -3.093539

iter 7 value -3.093697

iter 8 value -3.093833

iter 9 value -3.093892

iter 10 value -3.093911

iter 11 value -3.093936

iter 12 value -3.093984

iter 13 value -3.094011

iter 14 value -3.094024

iter 15 value -3.094034

iter 16 value -3.094060

iter 17 value -3.094071

iter 18 value -3.094083

iter 19 value -3.094096

iter 20 value -3.094131

iter 21 value -3.094173

iter 22 value -3.094216

iter 23 value -3.094245

iter 24 value -3.094264

iter 25 value -3.094306

iter 26 value -3.094367

iter 27 value -3.094428

iter 28 value -3.094455

iter 29 value -3.094462

iter 30 value -3.094472

iter 31 value -3.094524

iter 32 value -3.094544

iter 33 value -3.094549

iter 34 value -3.094559

iter 35 value -3.094567

iter 36 value -3.094651

iter 37 value -3.094754

iter 38 value -3.094874

iter 39 value -3.094927

iter 40 value -3.094960

iter 41 value -3.095024

iter 42 value -3.095085

iter 43 value -3.095128

iter 44 value -3.095143

iter 45 value -3.095150

iter 46 value -3.095163

iter 47 value -3.095169

iter 48 value -3.095171

iter 49 value -3.095175

iter 50 value -3.095195

iter 51 value -3.095209

iter 52 value -3.095219

iter 53 value -3.095223

iter 54 value -3.095225

iter 55 value -3.095229

iter 56 value -3.095233

iter 57 value -3.095236

iter 58 value -3.095237

iter 59 value -3.095239

iter 60 value -3.095243

iter 61 value -3.095249

iter 62 value -3.095252

iter 63 value -3.095253

iter 64 value -3.095254

iter 65 value -3.095254

iter 66 value -3.095254

iter 67 value -3.095255

iter 68 value -3.095255

iter 69 value -3.095255

iter 70 value -3.095255

iter 71 value -3.095256

iter 72 value -3.095257

iter 73 value -3.095258

iter 74 value -3.095258

iter 75 value -3.095258

iter 76 value -3.095258

iter 77 value -3.095258

iter 77 value -3.095258

iter 77 value -3.095258

final value -3.095258

converged

initial value -3.090645

iter 2 value -3.090694

iter 3 value -3.090714

iter 4 value -3.090751

iter 5 value -3.090787

iter 6 value -3.090923

iter 7 value -3.091012

iter 8 value -3.091065

iter 9 value -3.091069

iter 10 value -3.091074

iter 11 value -3.091087

iter 12 value -3.091096

iter 13 value -3.091103

iter 14 value -3.091110

iter 15 value -3.091131

iter 16 value -3.091335

iter 17 value -3.091362

iter 18 value -3.091379

iter 19 value -3.091491

iter 20 value -3.091561

iter 21 value -3.091583

iter 22 value -3.091600

iter 23 value -3.091687

iter 24 value -3.091796

iter 25 value -3.092028

iter 26 value -3.092302

iter 27 value -3.093118

iter 28 value -3.093396

iter 29 value -3.095274

iter 30 value -3.095467

iter 31 value -3.095812

iter 32 value -3.095871

iter 33 value -3.095891

iter 34 value -3.096063

iter 35 value -3.096087

iter 36 value -3.096112

iter 37 value -3.096157

iter 38 value -3.096163

iter 39 value -3.096164

iter 40 value -3.096164

iter 41 value -3.096166

iter 42 value -3.096169

iter 43 value -3.096171

iter 44 value -3.096171

iter 45 value -3.096172

iter 46 value -3.096172

iter 46 value -3.096172

final value -3.096172

converged

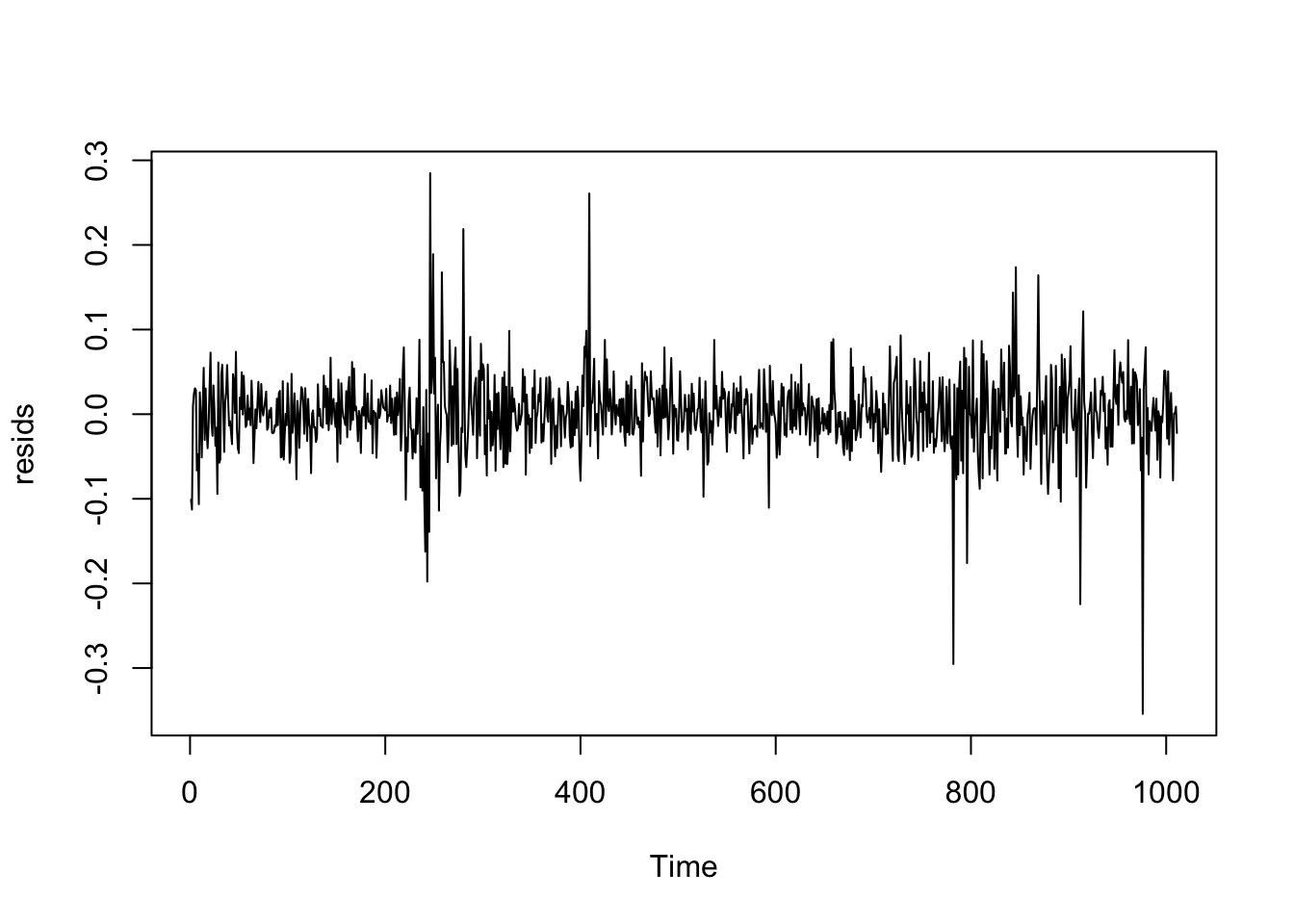

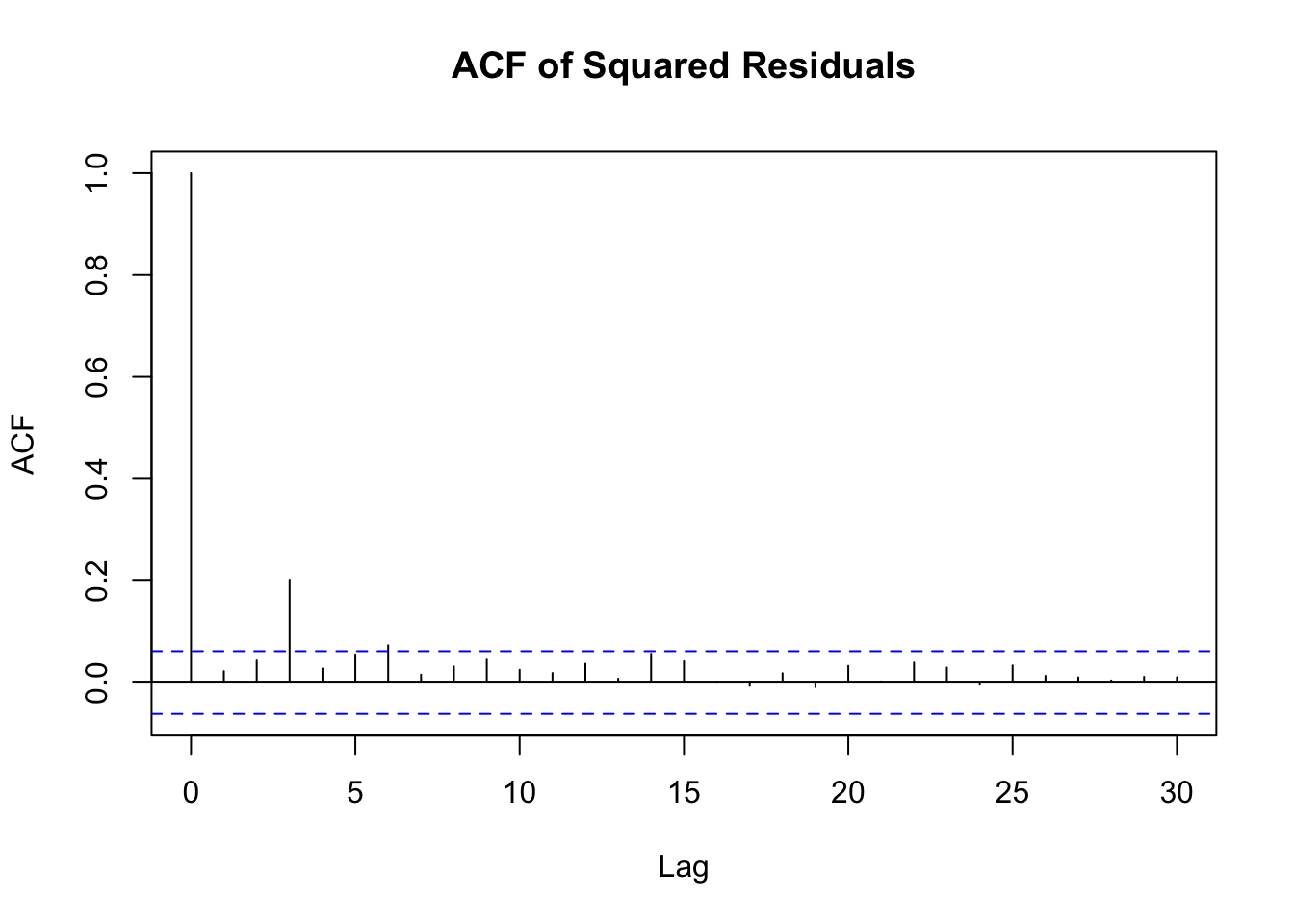

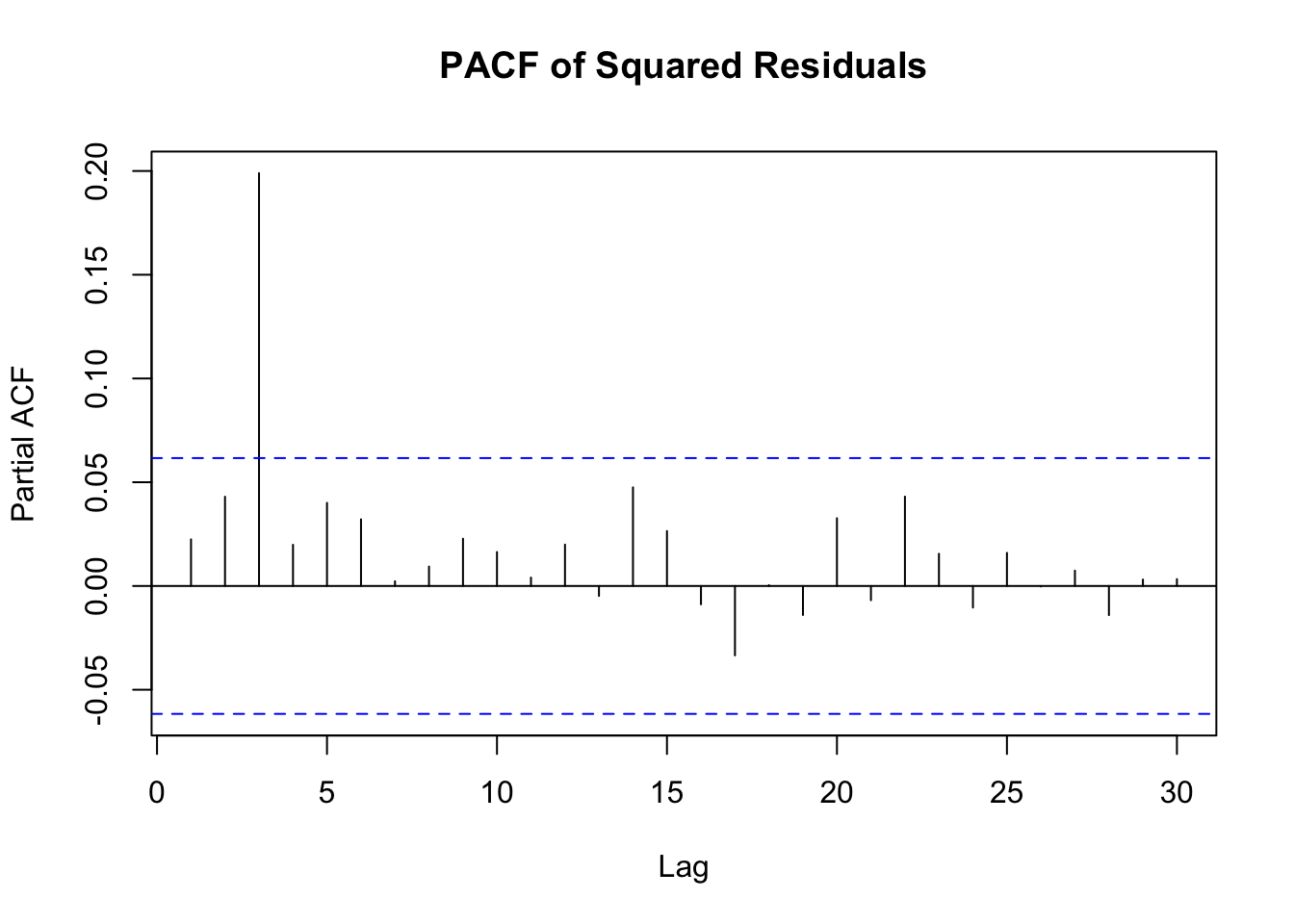

The standardized residuals plot shows that there is still significant volatility not yet modelled by the arma model. The acf and pacf plots of squared residuals both have significant correlation at the first few lags indicating that a garch model would be a good fit for the data. In addition the Arch Test has a p-value less than 0.05 so we can conclude that there are arch affects in the residuals.

Garch Model of (3,1) has the lowest AIC, however after looking at the significance of the coefficients of the model I determined that a GARCH(1,1) is the best model to fit this series. The Ljung-Box Test p-values are all above 0.05 indicating that there is no significant autocorrelation at various lags which is a sign of a good model.

Code

model <-list() ## set countercc <-1for (p in1:7) {for (q in1:7) {model[[cc]] <-garch(resids,order=c(q,p),trace=F)cc <- cc +1}} ## get AIC values for model evaluationGARCH_AIC <-sapply(model, AIC) ## model with lowest AIC is the bestwhich(GARCH_AIC ==min(GARCH_AIC))

The GARCH(1,1) model was the best fit for this data. It performs well on the Ljung-Box Test and does not have significant autocorrelation at any of the lags. The model still has high variation, indicating the need for more data. LYFT stock has only been publicly traded since March 2019, which is only a small dataset. Once LYFT has been traded for longer this analysis will be better able to forecast variation in the returns of its stock price.